There are many avenues for financing when it comes to buying and selling land. One less traditional way to finance your next deal is owner financing. Owner financing is worth exploring in many situations, whether you are selling a large, high-value property, a unique or remote piece of land, or if you are a buyer who may not qualify for a traditional bank mortgage. Owner financing can make the transaction faster and more flexible and, depending on your circumstances, could be an ideal solution for buyers and sellers.

Contents

What is Owner Financing in Real Estate?

Owner Financing vs. Traditional Bank Loan

Types of Owner Financing

Who Holds the Title in Owner Financing?

How Long is the Term for an Owner-Financed Sale?

Pros and Cons of Owner Financing Land Sales

Checklist Steps Before Entering an Owner-Financed Land Deal

Owner Financing FAQs

What is Owner Financing in Real Estate?

With owner financing — also known as seller financing — the seller of the land also acts as the lender. Rather than paying the full price upfront or going the route of a traditional bank-backed mortgage, the property buyer agrees to make payments over time directly to the landowner.

Like a mortgage from a bank, the buyer and seller agree on a down payment, the amount of monthly payments, the interest rate, and the length of the financing term. Then both parties sign a promissory note outlining the agreed-upon terms. The seller typically holds on to the title until the property is paid in full.

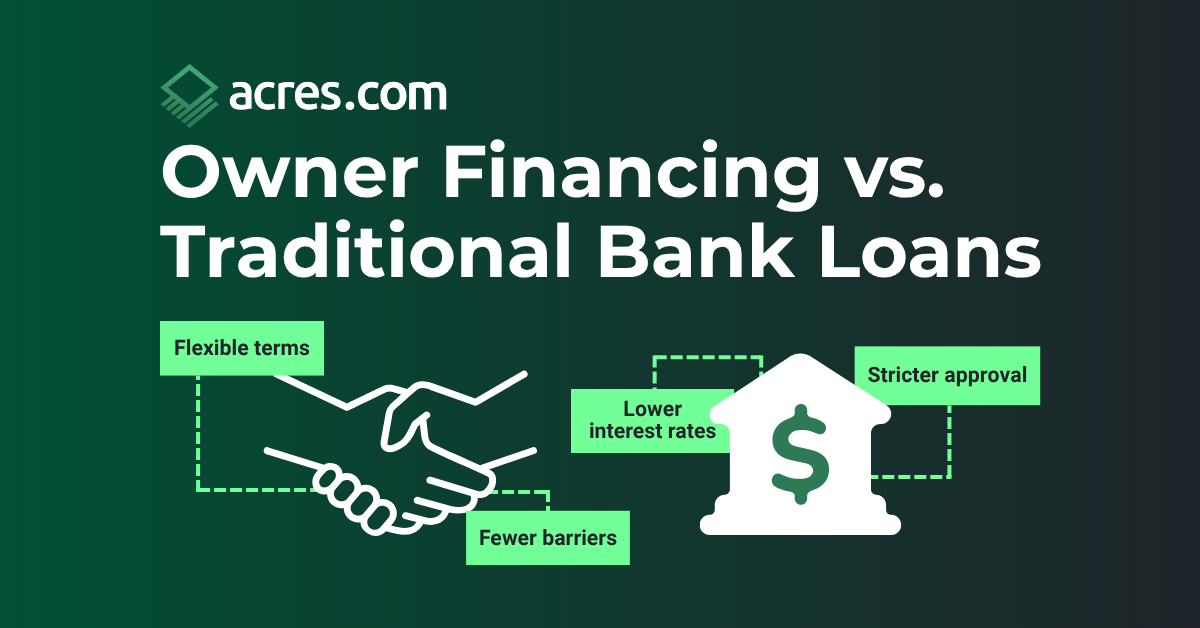

Owner Financing vs Traditional Bank Loan

|

Feature

|

Traditional Mortgage |

Owner Financing |

| Lender |

Bank or institutional lender |

Property seller

|

|

Approval Process

|

Credit, income, underwriting

|

Negotiated between buyer and seller |

|

Title Transfer

|

At closing |

Often delayed until full payment |

|

Interest Rates

|

Lower, regulated |

Higher but negotiable |

|

Loan Term

|

15, 20, 30 years |

Often shorter with a balloon payment |

Types of Owner Financing

Owner financing may be structured in a few different ways, including the most common:

Land Contract

In a land contract, the seller retains legal ownership until the buyer pays off the full amount. The buyer, however, is typically responsible for the property's upkeep and taxes during this time. In a traditional land contract, the buyer can build equity and refinance.

Wrap-Around Contract

In a wrap-around contract, the seller pays their existing mortgage using the buyer’s payments and keeps the difference as profit.

Lease-Purchase Agreement

This contract allows the buyer to lease the land for a set period with the option to buy it at the end. A portion of the lease payments may go toward the eventual purchase price. The tenant usually takes responsibility for maintenance, taxes, and insurance, and the sale occurs once the lease ends.

Each agreement type has specific rules regarding who holds the title, which can affect the rights and obligations of both the buyer and the seller.

Who Holds the Title in Owner Financing?

In most cases of owner financing, the seller will keep the title until the buyer fully pays off the loan. Before entering into an owner financing agreement, it is also important for buyers to pay for a title search on the property to ensure that the seller is indeed the title holder and is in a position to sell the property and hand over the title once all payments have been made.

How Long is the Term for an Owner-Financed Sale?

Owner-financed deals are typically short-term loans. To keep monthly payments low, the loan is amortized (or distributed across a repayment schedule) over 30 years with a large balloon payment due after only five or 10 years.

Often with balloon payment terms, the buyer never intends to fulfill the full terms of the loan. Instead, the buyer builds equity or secures more traditional financing in the short term and then pays off the original loan long before the balloon payment is due.

Note: The Dodd-Frank Wall Street Reform and Consumer Protection Act now prohibits balloon payments for residential mortgage transactions when the buyer plans to live on the property. However, the Dodd-Frank Act does not apply to commercial real estate, vacant land, or investment properties.

That being said, consulting with a qualified real estate attorney for owner-financed transactions is always advisable.

Pros and Cons of Owner Financing Land Sales

In many situations, owner financing is the best option for buyers if traditional financing isn't possible. As you explore if owner financing is right for your circumstances, take a look at the pros and cons.

| |

Pros |

Cons

|

| Buyer |

- Alternative when bank won’t finance

- Flexible terms, negotiation possible

- Faster closing (no bank underwriting)

- Potential to build equity

|

- Higher interest/cost

- Shorter terms and balloon risk

- Risk of losing property (default)

- Limited resale or transfer options before payoff

|

| Seller |

- Wider pool of buyers

- Ability to charge premium price

- Income stream/interest income

- Faster sale in more challenging markets

|

- Risk of buyer default

- Costs & hassle of foreclosure

- Delayed full capital return

- Liability/maintenance obligations until title passes

|

Example Scenario: Let’s say a Seller has a 50‑acre lot he can’t sell easily through banks. A Buyer offers $200,000, puts $20,000 down, and proposes a 10% interest rate, amortized over 25 years but due in 8 years (balloon). Sam agrees. Over the next 8 years Bob makes payments; at the 8th year, Bob must either refinance, pay the balance, or default. The Seller’s upside is more buyers, interest income, but his risk is the legal and procedural burden if the Buyer stops paying.

Land Diligence Checklist Before Entering an Owner-Financed Deal

Before diving into an owner-financed land purchase, it’s essential to go beyond the paperwork and analyze the land itself. All of these steps can be achieved by using Acres.com’s complete land research and mapping platform. Here's a due diligence checklist to help ensure you're making an informed investment:

- Verify Property Lines: Use Acres to confirm property lines and identify any discrepancies, encroachments, or unclear access points. While this does not replace a survey, it can help you flag potential issues earlier.

- Review Recent Comparable Sales: Compare recent sales of similar parcels in the area to make sure the purchase price is fair. Acres can help you surface recent sales quickly and accurately.

- Check Land Use History: Investigate how the land has been used over time. Things like agricultural use, mining activity, or previous development attempts can influence value.

- Assess Topography and Soil: Look at slope, flood zones, and soil composition to understand whether the land suits your intended use, whether for farming, building, or recreation.

- Confirm Zoning and Restrictions: Review local zoning regulations, conservation easements, or land use restrictions that could limit what you can do with the property.

- Evaluate Access and Utilities: Does the parcel have legal road access? Are power lines nearby? Lack of access or infrastructure can drastically affect value and development feasibility.

Note: While land diligence helps you make an informed purchase, it's still essential to work with professionals. A real estate attorney can review contract terms, and a financial advisor or tax professional can guide you on loan structure and long-term implications.

Owner Financing FAQs

Q: What is owner financing?

A: Owner financing, also known as seller financing, is an agreement in which the seller of the property also acts as the lender instead of the buyer securing a traditional bank-backed loan. The buyer pays for the property over time in installments directly to the seller.

Q: How does owner financing work?

A: In an owner financing agreement, the buyer and seller agree on key terms such as the down payment, monthly payment amounts, interest rate, and loan duration. A promissory note is signed, and the seller typically retains the title until the buyer has paid off the loan.

Q: What should I do before agreeing to an owner-financed land deal?

A: Do your land diligence. Even with flexible terms, it’s crucial to verify boundaries, comparable sales, past land use, and access. Acres helps you evaluate a property quickly with instant access to parcel-level insights and nearby sales.

Q: Who holds the title in owner financing?

A: In most cases, the seller will remain in possession of the title until all payments have been made or the buyer secures more traditional financing to pay off the remainder of the loan.

Q: What types of owner financing are available?

A: There are several types of owner-financing arrangements, including land contracts, wrap-around contracts, and lease-purchase agreements.

Q: What should buyers consider when buying owner-financed property?

A: It can be a good option for buyers who may not qualify for traditional loans. They can still purchase land with more flexible terms and a quicker and easier process. However, there are typically higher interest rates than a bank loan and shorter payment terms. Plus, you can risk losing the property and any equity if you default on payments.

Q: What should sellers consider when offering owner financing?

A: Owner financing can increase the pool of buyers in competitive markets. Since buyers may not qualify for traditional loans, they may be willing to pay a higher sales price, and monthly payments are an added revenue stream. However, if the buyer defaults, you may need to go through the hassle of foreclosure, and since the loan delays the full payment, you cannot invest that capital elsewhere.

Q: Should I consult a real estate attorney for owner financing agreements?

A: Yes. You should consult a qualified real estate attorney when considering owner financing. They can help clarify the legal aspects of the agreement and address all necessary details, protecting both parties in the long term and providing peace of mind about the transaction.

Final Thoughts

For buyers, owner financing can offer an alternative means to purchase land when traditional financing isn’t an option. For sellers, it can broaden the pool of potential buyers and create an alternative income stream.

Ultimately, the choice to use owner financing depends on the specific circumstances of the individual buyers and sellers. Both parties must carefully weigh the risks and benefits, ensuring they fully understand the terms of the agreement before committing.

Although owner financing bypasses a traditional mortgage lender, consulting a real estate attorney is advisable to address all details. With careful planning, it can be a flexible and beneficial arrangement for both parties.