Development

When “Out of the Flood Zone” Isn’t Enough

Identify critical subsurface risks in land acquisition with Acres. Learn why flood zone status alone isn’t enough for successful development.

Learn how to read a FEMA flood zone map for site selection. Understand flood zone designations, what they mean for land development, and how to run a floodplain parcel lookup before you buy.

Flood damage is the most common and costly natural disaster in the United States, and many buyers never check the map before they close. According to FEMA, flooding causes more than $8 billion in damage annually in the U.S., yet a significant portion of that loss falls on properties where the risk was visible on public records before the purchase was made.

If you're evaluating land for development, agriculture, or investment, a FEMA flood zone map is one of the first documents you need to pull. It tells you whether a parcel sits in a regulated flood zone, which designation applies, and what that means for your insurance costs, permitting timeline, and development feasibility.

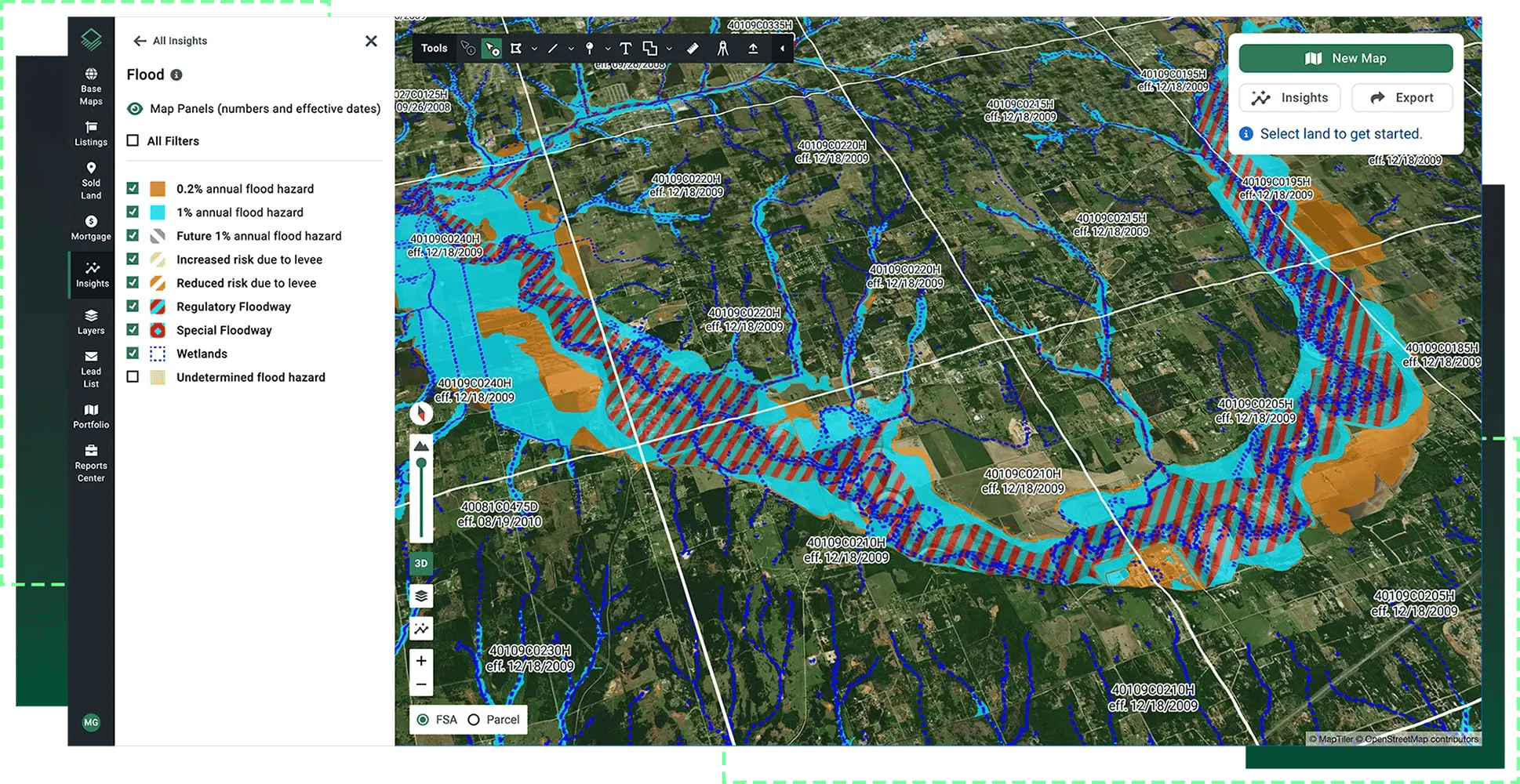

With Acres.com, flood zone classification surfaces automatically alongside ownership, zoning, and parcel details for any property you're screening. This post breaks down exactly how to read a floodplain map and what each FEMA zone classification means for site selection.

The Importance of Reading Flood Maps for Site Selection and Development

What Is a FEMA Flood Zone Map?

FEMA Flood Zone Designations: A Full Breakdown

How to Read a Floodplain Map for Site Selection

What FEMA Zones Mean for Flood Zone Land Development

Flood Zone Site Selection: Red Flags and Workable Situations

How Acres Handles Flood Zone Data at Scale

Most land buyers understand that flood zones matter. Fewer understand why a single-letter zone designation can be the difference between a viable parcel and a deal that never gets built or financed.

FEMA administers the National Flood Insurance Program (NFIP) and produces the Flood Insurance Rate Maps (FIRMs) that serve as the legal boundary for flood zone regulation in the U.S. While there are roughly 3.5 million miles of streams and rivers across the country, FEMA has mapped over 1.1 million miles of them, outlining the precise boundaries that determine mandatory flood insurance requirements, federal lending rules, and local building permit conditions.

The challenge is that FIRMs are dense, technical documents. For anyone buying rural land or evaluating parcels at scale, floodplain map site selection requires knowing which zones trigger regulated development thresholds and which ones leave your optionality intact. Understanding the FEMA flood zone map system is not optional. It's foundational due diligence.

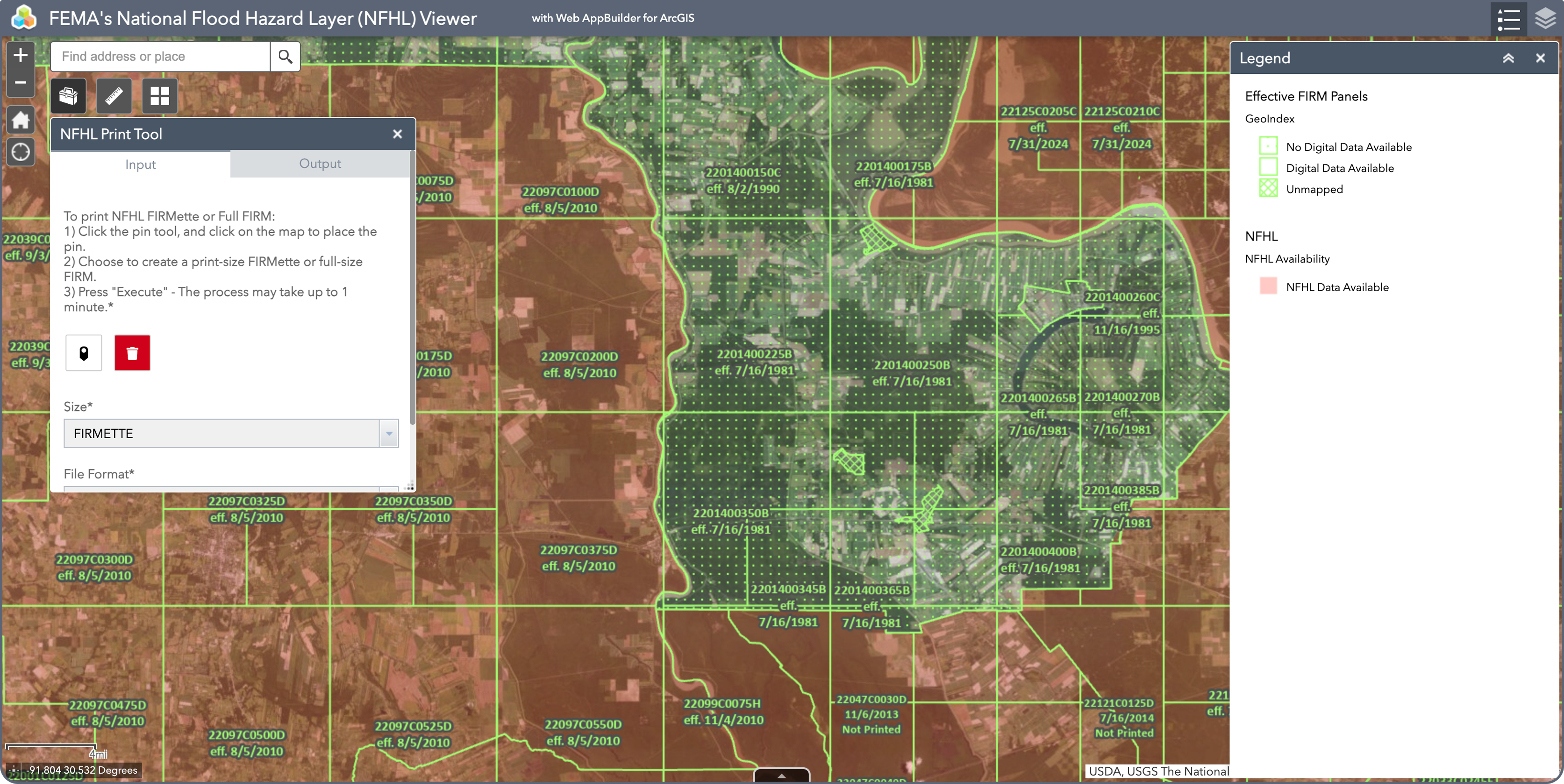

A FEMA flood zone map is a community-level document that shows the boundaries of flood hazard areas, the base flood elevation (BFE) for most zones, and the regulatory framework that governs land use within those boundaries.

FIRMs are produced by FEMA's Flood Map Service Center and are accessible to the public at no cost. They exist in both paper format and as digital GIS layers through the National Flood Hazard Layer (NFHL). For many site selection workflows, the digital NFHL is the practical tool. It allows parcel-level lookup and can be layered with ownership, zoning, and other due diligence data.

Every parcel in a mapped community falls into a flood zone designation. These designations are divided into two fundamental categories: Special Flood Hazard Areas (SFHAs) and non-SFHAs. That boundary is the most consequential line on any floodplain map.

Source: FEMA National Flood Hazard Layer

The following table covers the zone designations you'll encounter most frequently on a FEMA flood zone map, along with their risk level and practical implications for land acquisition and development.

| Zone | Common Name | Risk Level | Key Notes |

| Zone A | Special Flood Hazard Area | High | No BFE shown; mandatory flood insurance |

| Zone AE | Special Flood Hazard Area | High | BFE provided; most common high-risk zone |

| Zone AH | Ponding Hazard | High | Shallow flooding; BFE shown in feet |

| Zone AO | Sheet Flow Area | High | Shallow flooding; depth shown in feet |

| Zone VE | Coastal High Hazard | Very High | Includes wave action; strictest standards |

| Zone X (shaded) | Moderate Risk | Moderate | 0.2% annual chance flood; no mandatory insurance |

| Zone X (unshaded) | Minimal Risk | Low | Outside 500-year floodplain |

| Zone D | Undetermined Risk | Unknown |

No flood study conducted on this area |

Zones A, AE, AH, AO, and VE all fall within the Special Flood Hazard Area (SFHA). The SFHA is defined as land with a 1% annual chance of flooding, commonly referred to as the 100-year floodplain. Federally backed mortgage lenders are required by law to mandate flood insurance on any structure within an SFHA, and most local jurisdictions require FEMA-compliant permits for any development within these boundaries.

Zone X (shaded) represents moderate flood risk, the 500-year floodplain, and carries no mandatory federal insurance requirement. Zone X (unshaded) indicates minimal risk outside the 500-year boundary. Zone D is used where no flood study has been conducted and risk is undetermined, which carries its own underwriting implications.

Running a floodplain parcel lookup starts with identifying the effective FIRM panel for your target parcel, confirming the zone designation, and cross-referencing the BFE where applicable. For multi-parcel workflows or regional screening, the NFHL is available as a downloadable GIS layer or through API access.

Here's what to identify on a FIRM when evaluating land:

Locate the parcel on the map and confirm which zone letter applies. Any A- or V-prefix zone places the parcel in the SFHA.

Acres Tip: Search any address or parcel on Acres.com and the flood zone classification surfaces automatically alongside ownership, zoning, and parcel details. No separate portal visit needed.

Present in AE, AH, and VE zones. BFE is the elevation (in feet above sea level) that floodwaters are expected to reach in a 1% annual chance event. Any structure must be built at or above BFE.

Within Zone AE, the floodway is the channel and adjacent land reserved for floodwater passage. Development in a floodway faces the strictest restrictions and often cannot be permitted at all.

FIRMs are issued by panel. Check the effective date. Older panels may predate recent community growth or remapping efforts. Always confirm the current effective FIRM before closing.

If a parcel appears in a high-risk zone but sits physically above BFE, a LOMA can formally remove it from the SFHA. Check FEMA's LOMA database to confirm whether an amendment is already on file.

Rather than pulling flood zone data from multiple government portals and cross-referencing ownership records separately, Acres brings flood zone classification, ownership history, zoning, and parcel context into a single view. For teams running high-volume site selection, that integration compresses what would otherwise take days of manual lookups into a single search.

Zone designation is not just a disclosure issue. It shapes the entire development timeline and cost structure for a parcel. Here is what you need to know:

The Permitting Workflow: For properties in High-Risk SFHAs (like Zones A and AE), you cannot just build. Local jurisdictions require an initial Elevation Certificate based on your preliminary construction drawings just to secure a building permit. Once construction is finished, you must submit a definitive, post-construction Elevation Certificate before a final Certificate of Occupancy is granted.

For more details, technical specifications, and official regulatory guidelines, visit the official FEMA site.

Floodway designation within Zone AE typically prevents any development that raises BFE. A parcel that is entirely or predominantly in a floodway usually cannot be built to any meaningful density. Combined with wetland designations, which often overlap in the same areas, these parcels may carry conservation value but rarely carry development feasibility.

Coastal Zone VE parcels without substantial upland acreage face stacked regulatory requirements from FEMA, state coastal programs, and Army Corps of Engineers Section 404 jurisdiction. The permitting runway alone can run multiple years, and many projects in these zones fail at the permit stage.

A parcel with a small SFHA footprint, say, a creek corridor crossing the back 10% of a 200-acre tract, rarely constrains a full development program. The key is understanding what percentage of the net developable area is impacted, whether the site design can absorb the setback, and whether local floodplain regulations allow any fill or mitigation to reduce the footprint.

Zone X parcels are often incorrectly treated as equivalent to SFHA zones. They are not. Flood risk exists, and insurance is advisable, but the mandatory insurance and permitting requirements that govern SFHAs do not apply. For land acquisition at scale, understanding the difference between Zone X shaded and Zone AE is not a minor technicality. It is the boundary between a standard development process and a substantially more complex one.

For teams evaluating multiple parcels simultaneously, manually cross-referencing flood designations with ownership and zoning data is time-intensive. Acres integrates FEMA flood zone and wetland designations directly onto the map, so every parcel lookup surfaces flood zone classification alongside ownership, soil, zoning, and infrastructure data in a single view.

When Acres users screen land for acquisition targets, flood zone risk is flagged instantly. For development teams running high-volume site selection, that integration compresses weeks of manual flood zone screening into minutes.

A FEMA flood zone map is a decision document, not a formality. Zone designation determines mandatory insurance, federal lending requirements, permitting conditions, and the practical ceiling on what a site can support. The SFHA boundary is the threshold where regulation intensifies and development costs climb.

For land acquisition, running a floodplain parcel lookup before you get to contract is the minimum standard. Confirm the zone designation, identify the BFE if applicable, check for floodway overlaps, and verify the effective FIRM panel date. The information is public, free, and available. It belongs in your site selection checklist before any development begins.

Connect with our team to see how Acres can help you explore flood zone data alongside ownership, zoning, and parcel details for any property with speed and confidence.

Identify critical subsurface risks in land acquisition with Acres. Learn why flood zone status alone isn’t enough for successful development.

Discover Bay County, Florida's zoning map with Acres.com. Explore zoning laws, classifications, and land use planning to make informed property...

Explore Miami’s zoning map and learn how the Miami 21 code shapes sustainable, mixed-use development. Access parcel-level zoning data with Acres.