While many land transactions happen between neighboring operators, farmers, and individual investors, a quieter class of buyer has been accumulating acreage across the United States, and they rarely show up on the open market.

Institutions like pension funds, insurance companies, sovereign wealth funds, and private equity managers are driving some of the largest land purchases in the country right now. Their acquisitions don't always generate headlines, and that's partly the point.

If you work in land (buying, selling, or advising), understanding where institutional land buying is concentrated, and why, gives you a meaningful edge before deals show up in public records. Rather than piecing together ownership records, parcel data, and transaction history from separate sources, Acres.com consolidates all of it into a single view.

Contents

Why Institutional Investors Are Moving Into Land Right Now

The Four Land Types Attracting the Most Institutional Capital

What Signals Are Institutional Buyers Actually Tracking?

How Land Professionals Are Tracking Institutional Activity Before It's Public

The Bottom Line on Institutional Land Accumulation

Why Institutional Investors Are Moving Into Land Right Now

The U.S. farmland market totals more than 900 million acres, yet institutional ownership accounts for less than 1% of that total, compared to the 10 to 20% institutional ownership seen across other commercial real estate types.

Institutional land acquisition has accelerated for a straightforward reason: land behaves differently from every other asset class. During the 2008 to 2009 Great Financial Crisis, when the S&P 500 fell more than 46%, the NCREIF Farmland Index rose 17%. During the Q1 2020 COVID shock, when equities dropped 19.8%, farmland returned just -0.1%.

That kind of resilience has asset managers paying attention. Add chronic supply constraints, with U.S. farmland supply having declined nearly 20% since the 1960s, and you have a combination of scarcity and stability that draws long-duration capital in large volumes.

The result is institutional land buying at a scale that is already moving values in the most targeted markets.

The Four Land Types Attracting the Most Institutional Capital

1. Productive Row Crop Farmland: The Corn Belt and Northern Plains

The highest concentration of institutional farmland investment in the U.S. remains in the Midwest's core agricultural corridor: Illinois, Iowa, Indiana, Nebraska, and the Dakotas. These markets offer exactly what large-scale buyers want: reliable cash rents, documented soil productivity, and predictable yield histories.

According to the USDA's 2025 Land Values Summary, cropland averaged $5,830 per acre nationally, a 4.7% year-over-year increase from 2024. Michigan led the Lake States with an 8.2% gain, and Minnesota cropland climbed 7%. These aren't speculative gains, they reflect genuine demand pressure from institutional buyers parking long-term capital in proven agricultural ground.

The Teachers Insurance and Annuity Association of America (TIAA), through its asset management arm Nuveen, manages roughly $13.7 billion in global farmland and timberland assets. As the world’s largest manager of farmland, Nuveen has been one of the most active institutional buyers in the U.S. Corn Belt for over a decade.

State pension funds and sovereign wealth vehicles have followed the same playbook: acquire scale positions in high-productivity ground, lease to operators, and hold for appreciation.

The NCREIF Farmland Index, which tracks properties held on behalf of tax-exempt institutional investors, the great majority being pension funds, has delivered an average gross return of approximately 11.5% annually since its inception in 1991. Land professionals tracking these patterns use parcel-level ownership and transaction data to stay ahead of where institutional capital is concentrating.

2. Timberland: The Southeast and Pacific Northwest

Timberland investment has been institutional for longer than farmland, and the playbook is well established. Real estate investment trusts with multi-million-acre portfolios operate across Alabama, Arkansas, Georgia, Idaho, Louisiana, Mississippi, South Carolina, and Washington, managing timber harvests as long-duration, inflation-linked cash flows.

The Southeast continues to attract new capital because of low land costs relative to the Pacific Northwest, faster timber growth rates, and access to strong export markets. In 2024 alone, institutional-grade timberland acquisitions in Florida and Georgia totaled ~$22.8 million across 7,000 acres.

Timber also unlocks a secondary revenue stream that has become increasingly valuable: carbon credits. Forests held under institutional management are increasingly enrolled in verified carbon programs, layering ecosystem service income on top of harvest revenue. This dual income model has made timberland one of the more compelling large land purchases available to buyers operating on a 20-to-30-year investment horizon.

3. Solar and Renewable Energy Land: The Sun Belt and Appalachian Transition Zone

One of the fastest-moving categories in institutional land acquisition today isn't farmland at all, it's ground that can host utility-scale solar and wind development. Technology companies, energy infrastructure funds, and renewable energy developers are aggressively securing land in Texas, the Carolinas, Georgia, Virginia, and the Ohio River Valley.

The logic is straightforward: energy demand from AI infrastructure and data centers is accelerating faster than grid capacity can keep up. Data centers were the top target for institutional property investors in 2025 according to the Urban Land Institute/PwC Emerging Trends in Real Estate report. That demand creates a domino effect. Data center operators need renewable energy, and renewable energy developers need land.

Solar lease rates, often $500 to $2,000 per acre annually on 25-to-30-year contracts, have made marginal agricultural land financially attractive in ways that crop income can't match. Institutional funds are quietly tying up options on thousands of acres before local landowners fully understand the premium being offered. Teams screening sites for energy and data center land acquisition need infrastructure proximity data at the parcel level to move fast.

4. Transitional and Peri-Urban Land: Western Growth Corridors

Not all institutional land buying is rural. Large-scale investors have been accumulating transitional land on the outer edges of growing metros, particularly in the Phoenix, San Antonio, Raleigh-Durham, and Boise corridors. This category is distinct: buyers aren't purchasing it for agricultural production. They're purchasing it for what it will become.

Cascade Investment, the family office managing Bill Gates' assets, made one of the most visible plays in this category when it acquired a significant stake in approximately 24,800 acres of transitional land on the western edge of Phoenix.] The region's population growth trajectory makes that ground a long-duration bet on urban expansion.

In these markets, large land purchases often move quietly through LLC structures, with ownership obscured enough that local brokers only learn who bought the land after the transaction records.

What Signals Are Institutional Buyers Actually Tracking?

The markets that attract institutional land acquisition share a recognizable set of characteristics. Understanding what institutional buyers are underwriting helps land professionals anticipate where the next wave of capital could concentrate.

- Soil productivity scores. Institutional farmland underwriting starts with parcel-level soil productivity data. High Productivity Index (PI) or Corn Suitability Rating (CSR) scores are non-negotiable filters for row crop acquisitions. Rather than pulling this data from separate government databases, Acres brings soil productivity scores directly into each parcel view.

- Water access and rights. Irrigated ground commands significant premiums and draws disproportionate institutional interest, particularly in the High Plains and Pacific Northwest where water rights are legally defined and transferable.

- Infrastructure proximity. For solar and data center land, transmission line capacity and proximity to substations are as important as the parcel itself. Sites with existing high-voltage infrastructure nearby trade at meaningful premiums.

- Lease term and tenant quality. Institutional investors price land in part based on in-place income. Long-term leases with creditworthy operator-tenants can improve a deal's financing and valuation.

- Carbon and ESG eligibility. Investors managing funds with sustainability mandates are prioritizing ground eligible for conservation easements, carbon programs, or regenerative certification.

Tracking these signals across multiple markets simultaneously is exactly where most land professionals lose time. Rather than pulling data from county GIS portals, government databases, and separate deed records, Acres surfaces ownership patterns, deed transfer histories, zoning classifications, soil data, and environmental overlays in a single parcel view. See how land prospecting with complete parcel intelligence changes how fast your team can qualify a market.

How Land Professionals Are Tracking Institutional Activity Before It's Public

The challenge with institutional land buying isn't that it's invisible, it's that by the time a transaction shows up in public records, the opportunity has already closed. Staying ahead of institutional accumulation requires monitoring ownership patterns, deed transfers, LLC unmasking, and parcel-level data across markets simultaneously.

Acres gives land professionals the data infrastructure to do exactly that. With coverage across over 150 million parcels, Acres surfaces the signals that matter, organized around the same five factors institutional buyers actually underwrite:

- Soil productivity. Parcel-level soil quality data, including Productivity Index and Corn Suitability Rating scores, available directly within each parcel view.

- Water access. Water rights overlays and irrigation data to identify which parcels command the premiums institutional buyers target.

- Infrastructure proximity. Infrastructure proximity layers showing transmission line capacity and distance to substations, critical for solar and data center site screening.

- Ownership and transaction history. Ownership history, deed transfer records, and LLC-registered entity tracking, so you can spot accumulation patterns before they become public knowledge.

- Carbon and ESG eligibility. Environmental and zoning overlays that flag parcels eligible for conservation easements, carbon programs, or ESG-mandated investment criteria.

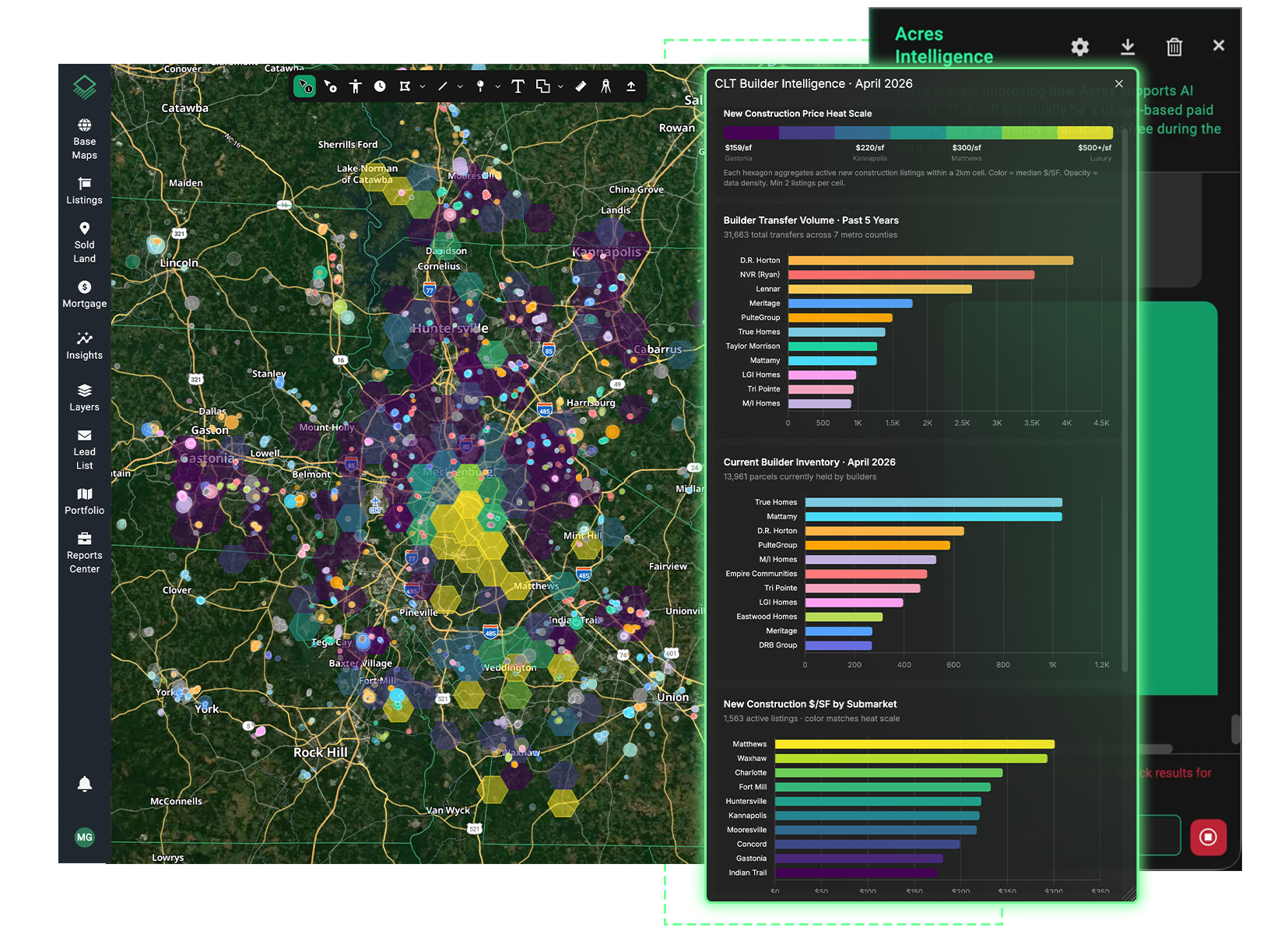

Teams use Acres Intelligence to describe the market signals they're watching and get answers fast, turning weeks of fragmented research into a focused view of where institutional money is moving.

Dashboard tracking market activity using Acres Intelligence. Example showing builder activity near Mecklenburg County, North Carolina.

The Bottom Line on Institutional Land Accumulation

Institutional buyers are not a distant or abstract force in the U.S. land market. They are active in the Corn Belt, the Southeast's timberland corridors, the Sun Belt's solar development zones, and the transitional fringes of the West's fastest-growing cities. Their capital is patient, their diligence is rigorous, and their acquisitions often precede value increases that independent buyers later pay full price for.

The clearest advantage any land professional can build right now is the ability to read these signals earlier than the competition. Where institutional money goes, market movement follows, and the window to act before institutional buyers lock up the best parcels is shorter than most land professionals expect.

See Where the Deals Are Happening

Contact our team and see how your team can explore ownership data, transaction history, parcel intelligence, and more for any market nationwide.